Break-Even Analysis Introduction: Calculation & Importance

The Significance of Learning Break-Even Analysis

Each organization begins its operations with one fundamental question:

“How much must be sold to avoid losses?”

The response to this question can be found through break-even analysis.

The primary function of break-even analysis is to provide businesses, new enterprises, entrepreneurs, and financial managers with knowledge of the specific level of activity at which the total cost is equal to the total revenue. This is a stage where there is neither profit nor loss; only the threshold point from which profits are made.

In whatever capacity an individual may be operating within the business world, whether as an entrepreneur, a financial manager, an employee in charge of managing the affairs of a particular enterprise, or a student of business finance, break-even analysis holds a crucial place.

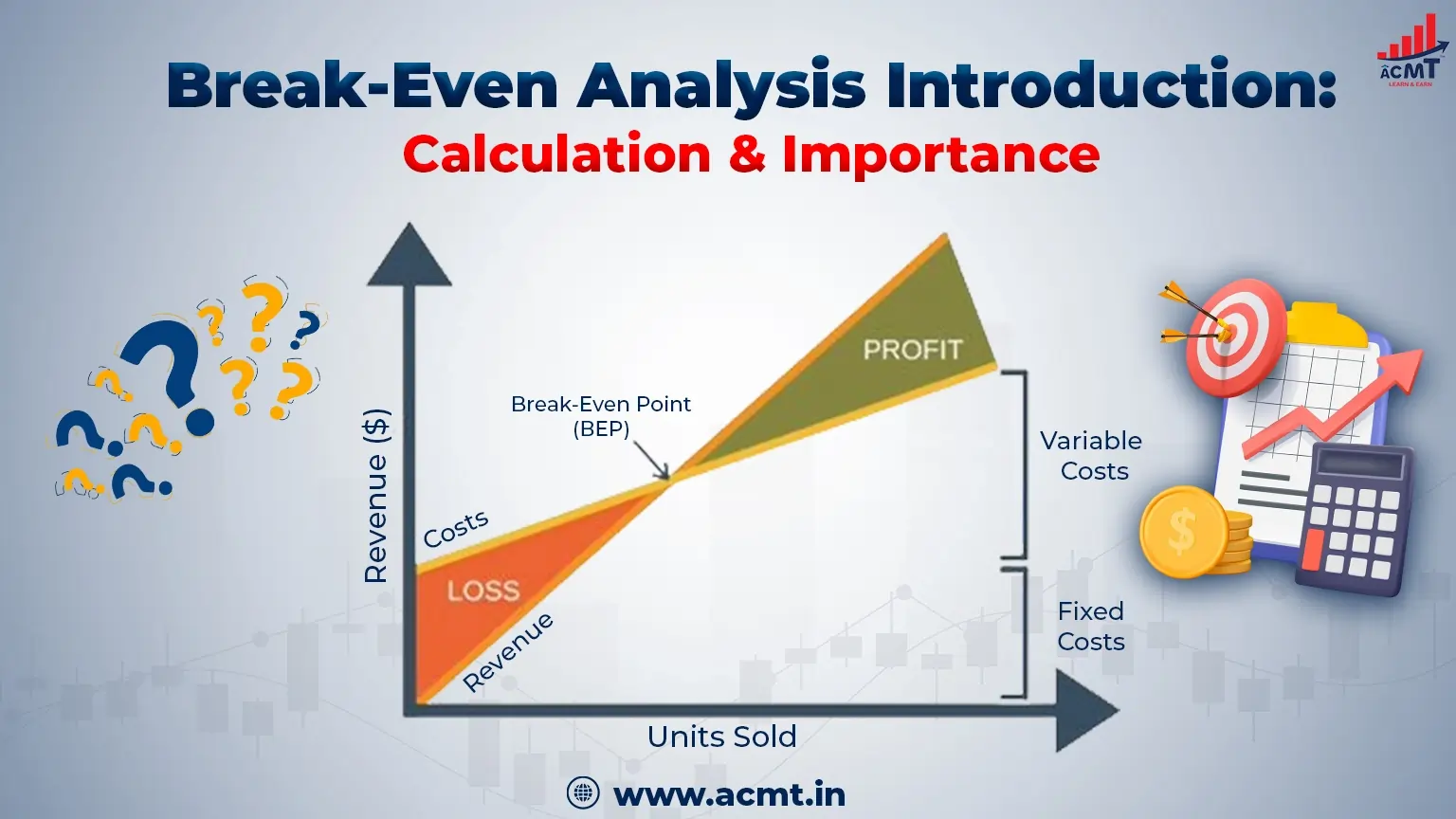

What Is Break-Even Analysis?

Break-even analysis refers to a financial calculation through which a firm can find out the minimum number of units required to be sold to make its revenues equal to costs.

This means that break-even analysis finds out the level at which:

Revenue = Cost

It is important to note that at this level, no profit or loss occurs.

This level is known as the Break-Even Point (BEP).

After achieving this level, each extra unit contributes to profits.

That’s why break-even analysis emerges as one of the most valuable tools for financial management.

Reasons for Using Break-Even Analysis by Businesses

In order to determine the financial viability of an enterprise, businesses must first make projections regarding their potential. Break-even analysis is one method used in this process.

The technique enables business leaders to know the amount of sales required for the organization to earn profits. This enhances price setting, production, and investment practices.

For instance, if a new firm needs to sell 2,000 units in order to break even, it can strategize on how to market the product.

Businesses do not operate without set targets.

Elements for a Break-Even Analysis

There are basically three major elements that are used for conducting a break-even analysis:

Fixed Costs

Fixed costs stay constant irrespective of production.

These include rent, salary, insurance, and other office-related costs. They have to be paid even when production comes to a halt.

Variable Costs

Variable costs will differ based on the production quantity.

They include the cost of raw material, packaging, electricity during the manufacturing process, and transportation costs.

More production means higher variable costs.

Selling Price per Unit

It is the price at which the product is sold to the consumer.

High selling price lowers the break-even point, and vice versa.

With knowledge of these three basic elements, conducting a break-even analysis becomes very easy.

Contribution Margin: The Key Idea in Break-Even Analysis

The idea of contribution margin forms the basis of break-even analysis. It shows the amount of contribution per unit sold in covering fixed costs minus variable costs.

After the coverage of fixed costs, the contribution equals profits.

Formula for Contribution Margin

Contribution Per Unit = Selling Price Per Unit – Variable Cost Per Unit

It follows that:

Contribution = SP – VC

An increase in contribution margin results in a lower break-even point.

A decrease in contribution margin leads to an increase in the break-even point.

For this reason, businesses strive to raise their contribution margins through higher selling prices or lower variable costs.

Calculating the Break-Even Point in Step-by-Step

Here’s how you can calculate the break-even point in steps through an example.

Step 1: Find out Fixed Costs –

Firstly, determine the fixed costs. This will include all those costs that remain the same irrespective of the level of production.

For example, Company A has:

Rent Expense = ₹4,00,000

Salary Expense = ₹2,00,000

Therefore,

Fixed Cost = ₹6,00,000

The total amount needs to be recovered first before making profits.

Step 2: Determine the Variable Cost Per Unit –

Then, find out the cost incurred per unit in terms of variable costs. Variable costs increase/decrease depending on the volume of production.

The variable costs are:

Raw Material = ₹8,000 per unit

Packaging = ₹2,000 per unit

Hence,

Variable Cost per Unit = ₹10,000

It is the cost incurred to produce one unit.

Step 3: Determine Selling Price per Unit –

Next, determine the selling price per unit. The selling price must be greater than the variable cost to ensure that every sale helps to recover the fixed cost.

Assume the selling price per unit is:

Selling Price per Unit = ₹16,000

Step 4: Compute the Break-Even Point –

First, compute the contribution per unit:

Contribution = Selling Price – Variable Cost

Contribution = 16,000 – 10,000

Contribution = ₹6,000

Using the break-even equation:

Break-Even Point (Units) = Fixed Cost ÷ Contribution

= 6,00,000 ÷ 6,000

= 100 units

This would mean that the company will have to sell 100 units in order to cover its expenses. This is the point where profit-making begins.

Break-Even Analysis Application in Daily Life

Taking the example of Company a mentioned above, let us use the equation and analyze how cost-volume-profit works in practical terms.

First, find out Contribution Margin per unit by applying the following formula: Contribution Margin = Selling price – Variable Cost per unit = ₹16,000 – ₹10,000 = ₹6,000. Second, compute the Break-Even Point (units) through the following equation: Break-Even Point (units) = Fixed Cost ÷ Contribution Margin = ₹6,00,000 ÷ ₹6,000 = 100 units. Lastly, determine Break-Even Point (revenue) through the application of the following formula: Break-Even Point (Revenue) = Break-even Units x Selling Price = 100 x ₹16,000 = ₹16,00,000. The result shows that the firm should be able to sell 100 units or earn ₹16,00,000 in revenue in order to reach.

The Significance of Break-Even Analysis in Strategic Management

Break-even analysis assumes great importance in strategic management. Through break-even analysis, companies are able to gauge their risks prior to making any investments.

Businesses can determine whether the proposed business venture is viable based on their sales projections and break-even considerations.

If the expected sales fall below the break-even point, then the business venture needs to be adjusted.

This decreases the risk of financial unpredictability and unforeseen losses.

Importance of Break-even Analysis in Pricing Decisions

Support for Setting Prices Appropriately for Goods

Proper pricing is essential for profit generation. Too low prices may make it difficult for the company to meet its expenses, while too high prices reduce customer demand.

Break-even analysis assists in deciding on the lowest possible selling price that will not lead to losses.

If there is an increase in production expenses, firms can set their prices appropriately to generate profits.

How Break-Even Analysis Assists with Managing Business Risks

There are always risks associated with businesses. But through break-even analysis, the amount of risk can be determined.

Where the break-even margin is quite high, there is more pressure on the company to sell huge amounts of its product. Where it is low, the company can generate profits faster.

This information assists managers in making necessary decisions concerning production or marketing strategies.

Break-Even Analysis Importance for Start-ups

Start-up businesses always have restricted funds. It is necessary for them to be well-prepared in advance to prevent any initial losses.

Break-even analysis assists entrepreneurs in determining how soon their business will begin earning profits.

It also assists them in deciding if they need to invest more money, change their pricing strategy, or cut costs.

Thus, break-even analysis is crucial for start-up businesses.

Application of Break-Even Analysis in Investment Decisions

Investors assess the business’s profitability prior to investing their funds.

The break-even point aids investors in assessing how quickly the organization will recover its costs. When a business has a low break-even point, it suggests quicker profitability and fewer risk factors.

Thus, the business becomes more appealing to investors.

Use of Break-Even Analysis in the Manufacturing Industry

Break-even analysis is important for manufacturing industries since costs fluctuate with the volume of production.

They use the break-even analysis method to calculate the number of products required to produce monthly profits. It helps them identify whether increased production would lead to increased profit or losses. This enhances efficiency.

Importance of Break-even Analysis for Service Organizations

Break-even analysis need not be restricted only to manufacturing firms. Service organizations also find this tool beneficial.

The break-even point for a coaching institute will tell how many students should be enrolled to meet operational costs.

A consultancy organization can determine the number of projects it needs to take up before making a profit.

Benefits of Break-Even Analysis

There are many benefits associated with break-even analysis, which applies to all businesses, big or small.

Below are some techniques for using break-even analysis to help understand businesses better:

Determination of Sales Goals –

The break-even point analysis can be used by enterprises to know the number of units that should be sold in order for them to cover all their costs, so as to have an idea of realistic goals to set.

Cost Management –

Break-even analysis assists businesses in determining fixed and variable cost elements to see where there is unnecessary spending that should be cut off in order to decrease the break-even point.

Pricing Tactics –

It helps organizations in setting the most favorable product prices for their goods or services, such that the prices should cover all the costs involved and earn a profit.

Better Financial Awareness –

The break-even analysis tool gives a business the knowledge about cost structure, revenue needed, and the level of profits. This means that managers are able to determine the viability of a business project even before making any commitments.

As the formula is simple and effective, it can be adopted easily by different organizations in various sectors.

Break-Even Analysis Limitations

While break-even analysis is quite effective, it still has some disadvantages.

For one, it makes an assumption that the selling price will remain the same, which might not always be the case.

Also, it assumes that the amount produced will be equal to the amount sold, which is rarely the case in practice.

Nonetheless, break-even analysis proves to be quite effective if applied correctly under the appropriate assumptions.

Differences Between Break-Even Point and Profit Margin

| Basis of Difference | Break-Even Point (BEP) | Profit Margin |

| Definition | The break-even point is the level of sales where total revenue equals total cost. | Profit margin measures how much profit remains after covering all costs. |

| Purpose | Identifies when a business stops making losses. | Measures how efficiently a business generates profit. |

| Stage of Business | Occurs before profit begins. | Calculated after profit is generated. |

| Financial Position | Indicates a no-profit, no-loss situation. | Indicates actual earnings from sales. |

| Measurement Unit | Measured in units or sales revenue (₹). | Measured as a percentage (%). |

| Formula | Fixed Cost ÷ Contribution per Unit | Profit ÷ Sales × 100 |

| Focus Area | Cost recovery level | Profitability performance |

| Decision Support | Helps set minimum sales targets | Helps improve pricing and cost efficiency |

| Risk Indicator | The break-even point is the level of sales where total revenue equals total cost. | Shows business earning strength |

| Strategic Role | First step toward financial stability | Second step toward financial growth |

Conclusion:

Why Every Business Needs To Know About Break-Even Analysis

One of the most crucial methods in making financial decisions is the concept of break-even analysis. It enables a business to know its required sales for making profits. It makes planning less uncertain and more precise while enabling effective pricing and cost control.

Be it an entrepreneur, manager, businessman, or student of commerce, knowledge about break-even analysis comes in handy. This is because businesses make decisions on the basis of facts and figures.

And that’s why break-even analysis continues to remain an important part of finance and management.